If you’ve decided that you’d like to own a bar, then you normally have two options: build one from the ground up or buy an existing bar for sale. In this article we cover how to buy a bar in six steps. We’ll look at the reasons to buy rather than build, where to find a bar for sale, what to look for when buying a bar, what to negotiate for, and finally, how to seal the deal.

Buying a bar with no experience? If you have never worked in a bar, start by shadowing a bar owner or working part time as a bartender or server to get to know the business as an employee. Alternatively, talk to bar owners about the pros and cons about their work.

Ready to start your bar-buying journey? Here are the steps:

Step 1: Make Sure You’re Eligible to Be a Bar Owner

Operating a bar requires a liquor license. If you are buying an existing bar, the existing liquor license will likely be part of the sale. In order to transfer the bar to you, you’ll need to be eligible to hold a liquor license in your location. It’s best to know if you meet the requirements to hold a liquor license before you get too far into the bar purchase process.

In most states or counties (many areas issue liquor licenses by county), you’ll need to be a US citizen without a criminal history. You’ll need to pass a background check and submit a full set of fingerprints with your application.

Liquor license requirements vary by state or county. See our full article on how to get a liquor license for more information about how to get a license in your area.

Step 2: Determine the Kind of Bar You Want

This is an important first step, especially if you are buying a bar with no experience. After all, not all bars are alike. You need to find the kind of bar that is going to suit your personality, budget, the kind of people you want to associate with, even where you want to spend your days.

For example, a wine bar might be found in a trendy part of town or out closer to vineyards. It would appeal to a more genteel customer base and lends itself to events like wine tastings. By contrast, a dive bar may be in the center of town, cater to those more interested in drinking (rather than tasting), and feature live bands. A sports bar will probably have a small food menu, lots of large-screen TVs, and rowdy crowds on game night. Each will employ different personalities of people as well.

Only you can decide the type of bar you want. If you’re not sure, spend some time in each bar type and talk to owners about the pros and cons. This will help to narrow your search.

Step 3: Find a Bar

Once you know what you’re looking for, it’s time to find the perfect place. The best ways are with a business broker or through business sales sites. Then you’ll need to evaluate the listing for what they offer, price, and financial success factors (performance metrics).

How to Find a Bar

Work With a Broker

Business brokers specialize in helping to buy and sell businesses. They understand financial documents, tax returns, and other information that shows the success of a business. They often screen potential buyers because business searches take more time. However, they may have leads on upcoming bars for sale and can walk you through the market, leases, permitting process, and government regulations. You can find a broker through a Google search, your local Chamber of Commerce, or BusinessBroker.net.

Online Listings

If you have experience with business and want to find a bar on your own, there are online listings. Like real estate websites, they provide the basic information to get you started. We recommend using a lawyer to close the deal, regardless.

Determine What You Are Looking For

Bar listings include more than the asking price. You may also find dollar amounts for FF&E (furniture, fixtures, and equipment), and inventory. FF&E and inventory may or may not be included in the total asking price.

You should always be aware of what is being included in the asking price. Never assume something will transfer over with the bar. Sometimes, an owner may want to keep something, like their signature drink, to use at their next location. Or they may simply forget to include the bar’s Facebook page, which is a vital marketing tool. You may want to exclude something, like the old furniture; in which case, you may want to negotiate a lower price.

Here are things to consider:

- Equipment: This can include everything from taps to sound equipment. If you’re looking at a microbrewery, it’s especially important to know what brewing equipment is necessary. If you don’t have experience behind a bar, have someone with you to assess the equipment’s condition.

- Software and computers: Taking over a previous owner’s contracts for software means you don’t have to transfer information, which can be costly.

- Payment systems: Sometimes, you can take on any POS and payment systems the bar already uses. While this can save you retraining your staff, you may be taking on a long-term contract.

- Furnishings and small wares: Furnishings include everything from stools to pool tables to light fixtures. Small wares include plates, cups, and silverware. Before negotiating, check their wear as well as whether they fit your vision.

- Lease or property: Most bars are under long-term commercial lease contracts. If the owner does not own the location, you’ll be taking over the lease. Be sure to check the terms.

- Branding: If you want to keep the bar’s name and brand, you may need to pay to transfer the trademark.

- Liquor license: Be sure you understand what licenses you need for the bar and which are transferable with the sale. Some states have different licenses for hard liquor vs wine and beer, for example. Some licenses also dictate how the drink can be served—on location vs in to-go cups, for example.

- Permits and insurance policies: In addition to liquor licenses, you may need food or entertainment permits, as well as liability insurance and other policies. Find out what permits and insurance policies come with the purchase and which you can negotiate for.

- Business documents: Ask about the documents that establish the business entity such as incorporation documents that form the LLC as well as sales and payroll tax ID numbers.

- Intellectual property: Trademarks, copyrights, and trade secrets or signature recipes make your prospective bar what it is. Be sure these transfer.

- Operational documents: Using existing training materials, employee handbooks, and other governing documents spares you from reinventing the wheel. You’ll at least have a place to start even if you make changes.

- Product inventory: This covers everything from the beer on tap to the branded wine glasses—even cleaning supplies. You may not want all of it, especially branded products if you are rebranding.

Sometimes, you can get an option to buy the real estate along with the business. In that case, check out our guides on Buying vs Leasing Commercial Real Estate and Types of Commercial Real Estate Loans and How They Work.

Consider Each Potential Space

Visit the location as a customer to get a feel for the atmosphere, staff, and pros and cons of the bar. However, don’t over-visit or ask direct questions about the sale; you could make the employees nervous or hurt future relationships with them should you take over. Make note of problems—for example, a bartender serving a drink without checking ID—but don’t use them as bargaining chips. You could insult the owner and jeopardize your negotiations. Instead, use these as opportunities for improvement when you take over.

In addition to the financial metrics (discussed below), you need to consider the following:

- Why is the bar for sale? Talk to the owner about why they are leaving. Are sales falling? Is the customer base changing? Are they simply retiring and sad to leave? Ask them about their biggest challenges and rewards.

- What’s the bar’s reputation? Check Yelp and other review sites. Look for reviews in the local paper as well. Finally, ask customers what they like about the bar, but be discreet or let the owner know you are asking.

- How’s the neighborhood? How do neighboring businesses feel about the bar? Is there a lot of competition in the area? Is there a problem with parking?

Check the Bar’s Performance Metrics

Buying a bar is a business investment, so be sure you’re finding one that has a strong financial foundation. Look at the financial documents to back up what the ads or owners say about profits and losses. This may require signing a nondisclosure agreement (NDA).

Most business listings have some indicators like gross revenue, cash flow, or Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). Others you need to ask for. Some key performance indicators to ask about are:

- Gross Revenue: This is straight earnings, without consideration of expenses. While having high revenue is good, you have to look at costs. Binwise says that a good average gross profit is between 70% and 80%.

- EBITDA: This is useful when comparing different companies or determining profitability. Divide EBITDA by gross earnings to determine profit margins.

- Profit margin: Profit margin tells you what amount of top-line sales flow through to the restaurant’s bottom line. Binwise says that the average profit margin for a bar is 10%-15%. Wine bars earn 7%-10%, but can increase if you also sell wines and products on-premise.

- Cash flow: Like the name, this measures the flow of money in and out of your business, including revenue paid to the owner.

- Labor cost: This is how much you spend on staff wages and benefits, expressed as a percentage of total sales. Ideally, labor costs should be 30% or less where dining is included, 24% or less for standalone bars and nightclubs, according to TouchBistro.

- Liquor cost: Liquor costs average 18%-24%, according to Binwise. Wines can be as much as 30%.

- Food cost: Unless you are running a tavern or sports bar, where food is served as much as drink, this percentage should stay low.

- Prime cost: Prime costs are the controllable expenses it takes to run the shop, usually raw materials and direct labor.

- Online sales: These should be included in the documents, but check in case they are running this as a separate business. Wine bars and microbreweries often sell their products online, but even a local bar can make a little extra selling branded merchandise, especially if they have a fun or unique logo.

What the Metrics Tell You

Strong Metrics

Strong metrics mean a strong chance of success. In this case, you may want to consider how many changes you intend to make because the bar has already found a winning mix. This makes it a good choice for those wanting a business they can step into, but may not appeal to someone wanting more creative license.

Weak Metrics

If the metrics are weak, you need to do some research. A bad location is more of an issue than troublesome employees. A bad reputation might be the perfect opportunity for someone wanting to take a great location and rebuild it to their vision. If that’s you, consider the costs of making those changes, both in finances and in its effect on current staff and customers.

Step 4: Hire a Lawyer & Evaluate the Business

Buying a business is more complex than purchasing real estate. There are legal considerations from licenses to trademarked information. Your broker can only do so much, so you should hire a business attorney to protect your interests, ensure legality, and help you draft a clear contract with the current owners.

Some documents they may prepare include:

- Letter of Intent (LOI): An LOI states your intent to purchase the bar and sets out some basic terms and conditions of the purchase. An LOI may not be binding and can expire.

- Lease agreements: The bar may come with a long-term commercial lease, so have your attorney look it over for any red flags, like increased rent if the lease transfers.

- Asset purchase agreement (APA): Also referred to as a purchase contract or sales contract, the purchase agreement is the official document governing the business’s sale. It lays out terms like the agreed-upon purchase price and any conditions that must be met by either party to complete the sale. Some of these may be noted in the LOI or APA.

You can find an attorney through your local branch of the American Bar Association or a Google search, but be sure they have experience with bar purchases.

If you are on a tight budget, you can use a legal site that offers editable business documents. This can save you money. However, you’d do best to run these by an attorney to ensure they meet local law. Often these legal document sites have a way to find an attorney on their site.

Appraise the Business Value

In general, bars are valued by their sales (minus sales tax) or revenue plus inventory. Fast Business Valuations suggests 35% to 45% of annual sales + inventory. A broker can help you with valuation, which should be backed up by the bar’s financial documents.

Step 5: Get Funding

Determine Your Budget

Experts say that when buying a bar, you need to not only consider how much it costs for the purchase but be prepared to support the bar for the first year. The bar’s financial statements should give you an idea of how much you need to spend. Also consider:

- Salaries: Fair salaries are key to keeping good staff. If the staff is underpaid, this is a good time to fix that injustice. The US Bureau of Labor Statistics lists bartender salaries at $14.12/hour or $29,380/year; waitstaff at $14 per hour or $29,120/year (although this includes tips); DJs cost $500+ an hour.

- Marketing: You’ll want to put some extra effort into marketing, especially if you change the bar name or atmosphere. Toast suggests allocating 3% to 10% of your sales on marketing. Grand openings can cost $6,000 or more; about 20% of your first-year’s marketing budget.

- Drinks: If you are changing the menu to include specialty drinks or are upscaling the quality of the liquor, be sure to include this addition to your budget.

- Renovations and updates: You may need to update your space to meet codes that the previous owner was grandfathered into, or you may want to redecorate. This varies widely and you may want to get an estimate, but a good ballpark is $200-$250 per square foot. You may be able to negotiate for some of this expense to be paid for by the current owner.

Personal Investment

In general, you need to contribute 10% to 30% of the purchase price as a down payment. This is not part of the loan. It may have to come from your own funds, but you can also try other fundraising ideas like investors, crowdfunding, or loans from family and friends.

Loans

You’ll probably need a business acquisition loan or an SBA loan. SBA loans can be used to buy bars; they are backed by the government and have stricter requirements, but lower rates. Your local bank can help you find the right loan, or you can look at lending marketplaces or online banks. Regardless, you can apply for them through your local bank or via lending marketplaces. Some online banks specialize in small business loans. Check out our list of best banks for small business loans.

To apply for a business loan, you need a strong business plan, letters of recommendation, and financial statements for the business and yourself, including tax returns, and bank statements. You may have to personally guarantee a loan, especially if you are not purchasing the real estate of the bar (which you could use as collateral). SBAs require a credit score of 680 or higher, and higher scores can help decrease the interest rate.

Investors

You can use investors for the down payment or to purchase the bar in lieu of a loan. However, you need to offer them something in return. You might make them a full partner in the business, or you may offer a portion of the equity, profits, or other perks. Use a lawyer to draw up a legal document to protect yourself.

Step 6: Negotiate With the Seller

Now it’s time to negotiate a deal with the seller. Your broker or attorney can help you with this. You not only want to get the best price but be sure that you are getting everything you need in order to run the business immediately and successfully. Thus, take your time to get things right, even if it means going back and forth a few times.

Never assume something is included in the sale. If you need a license, ask. If you are taking over the lease, get the details (including whether the price is expected to rise with the change of hands). Will you take over the Facebook account? Be sure your final agreement includes passwords, key codes, and any other pieces of information you need to run the business.

Sign a Letter of Intent/Asset Purchase Agreement

Once you have hammered out the terms of the sale, you create and sign an LOI. This lines up the terms of sale and states that, barring any red flags, you will purchase the business and assets. You can make this non-binding and set an expiration date, such as if they do not provide documents in time or you cannot come to an agreement on any changes.

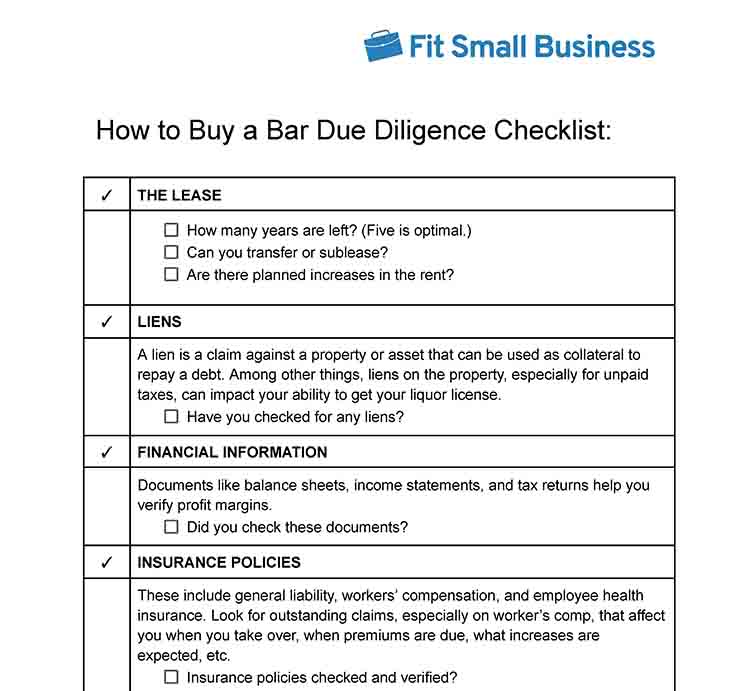

Do Your Due Diligence

Once you have the LOI, you can delve more deeply into all the financials and legal issues to look for any problems that make buying this bar a bad choice. The goal is to ensure the financial health and possibilities of success to your satisfaction.

To do this, you and your lawyer will examine the economic, legal, financial, and operational side of the business: verifying financial information, uncovering outstanding debts like unpaid taxes or accounts in arrears, verifying legal information, even checking for liens or potential lawsuits.

Download our free due diligence checklist for more details:

Thank you for downloading!

Hopefully, your due diligence won’t raise any red flags. However, if it does, you don’t have to quit. Renegotiate for a price adjustment or add some stipulations, like paying for building updates or including the recipe for the bar’s signature drink.

Step 7: Complete the Purchase

You’re almost there! Now comes the fun part—transitioning over to the new management (you!).

Transition & Closing Date

Transitioning a business can take weeks or more, especially when it comes to the paperwork of licenses. Use this time to get to know the business, the people, and the operations. The closing date is something you should discuss with the seller.

Here are some things you will need to do for a smooth transition:

- Update permits, policies, and vendor accounts with your contact information. (This can take weeks or even months—check with your state before setting a date.)

- Update the premises to meet new codes and schedule the appropriate inspections.

- Renovate if you want things done before you celebrate the changeover or start the plans if you’re going to do it after.

- Plan your marketing. Allow time for letting the public know about the change in ownership. This could mean press releases, social media posts, or planning a celebration on the closing day.

- Walk through the tasks the original owner typically does, both administrative and operational.

- Get some training on the software you personally will use (such as payroll software).

- Get introduced to the staff and the regular customers.

- Spend a day or two shadowing your staff and getting a feel for operations.

- Arrange for transfer of all software and passwords on the closing date.

Draft a Purchase Agreement

Your lawyer will draft a permanent and binding contract concerning the terms of sale. It should include everything in the LOI, any changes, and details like the transfer of accounts (including social media associated with the business), and who is paying for extra costs like closing fees, updates, and permit transfer fees. If the purchase agreement looks good, you pass it to the seller to have his attorney look it over.

Noncompete clause: You may want to include a noncompete clause to ensure the old owner does not go on to create a competing bar in your area. While some attorneys add this as a matter of course, others won’t unless requested.

Sign the Purchase Agreement

Finally! It’s time to sign the agreement. Then all that’s left is to transfer the money and get all the codes, keys, and passwords. Once that’s done, be sure to change the codes, locks, and passwords to ensure your security. Also make sure your new employees have your contact information.

And then celebrate! The adventure begins!

Pros & Cons of Buying a Bar

Owning a bar has great perks for those who like the scene: There’s the excitement of meeting new people, the promise that every day will bring something different, the satisfaction of providing a place where people can celebrate joys or drown sorrows, and a way to share your love of microbrews, fine wines, or exotic cocktails with an appreciative clientele. However, there are also long hours, the potential of dealing with inebriated and troublesome customers, and the pressure to make a business succeed.

If you are ready for all of that, purchasing a bar has some advantages over starting your own bar. You begin with an established location and customer base. You will probably know its strengths and weaknesses, giving you a clearer path for improvements. And, the investment is often less than if you are building from the ground up.

However, creating your own bar gives you greater creative control, and you don’t inherit someone else’s problems. Nor will you have to deal with disgruntled staff or customers if they don’t like your changes.

How to Buy a Bar Frequently Asked Questions (FAQs)

Can I make a living owning a bar?

According to Binwise, the average bar owner earns just below $40,000 per year, while ZipRecuiter statistics say it’s closer to $31,200. Bar managers, by contrast, earn an average of $53,000 per year.

How much does it cost to own a bar?

According to Binwise, the average monthly bar expenses are $24,200. Percentage-wise, it should be no more than 90% of your sales income. Wine bars that don’t sell merchandise may see smaller profit margins.

What should I watch out for when buying a bar?

Here are some red flags for when you buy a bar:

- Financial issues, including lack of profit or resistance to sharing their financials with you

- Outstanding debt

- High employee turnover

- Run-down equipment, furniture, or building

- Bad reputation or problems with the neighboring businesses

How often do bars fail?

Most failure rates concern new businesses, so if you are not making major changes, you have a higher chance of success if your new business was already doing well. Of new businesses, nightclub failures are as high as 75% on average, while food-serving bars have a failure rate closer to that of restaurants—about 30%.

Regardless of the type of bar, the main reason they fail is insufficient funds while getting established. Be sure you plan to support your new acquisition through the first few years of transition.

Bottom Line

Bars generally have high profit margins and are rewarding for people who enjoy networking and the excitement of being around people. If you’re ready to start your adventure as a bar owner, knowing how to buy a bar as opposed to starting one from scratch can save you money and get you in business faster.

Be sure you know what to look for, find a good attorney, and do your homework. Good luck!